Financial Education in the UK: Addressing the Gaps in Financial Literacy

Financial planning plays a crucial role in securing a stable future. However, many individuals struggle with even the basics. This raises the question—should financial education be improved at a fundamental level? Moreover, is the UK school curriculum effective in teaching children how to handle financial crises? In this article, we explore these pressing concerns.

The Financial Literacy Crisis in the UK

Millennials are known for their independence and desire to control various aspects of life. Yet, when it comes to managing personal finances, many young adults feel uncertain about their financial decisions. A recent study found that 93% of Britons believe they lack proper financial education. Additionally, nearly half (47%) think banks should provide better guidance on financial decision-making.

The Impact of Poor Financial Education

This study also revealed that 67% of UK residents feel under-confident when handling financial matters, while 68% admit to lacking financial awareness. These alarming statistics highlight the urgent need for a structured and comprehensive financial education program.

Why Financial Literacy Matters

Financial literacy is essential in everyday life. Young adults often struggle with crucial financial choices, including selecting credit cards, planning for retirement, and taking out loans. Although financial education has been a part of the UK curriculum since 2014, gaps in its effectiveness persist. Learning about taxes, budgeting, and debt management is not just beneficial but necessary for long-term financial stability.

Understanding Financial Illiteracy in the UK

- Financial Lives Survey results indicate that young adults (ages 18-24) consider themselves the least confident in financial decision-making.

- More than half of adults report that poor financial management negatively affects their mental health.

- Despite financial education becoming mandatory in 2014, implementation gaps remain.

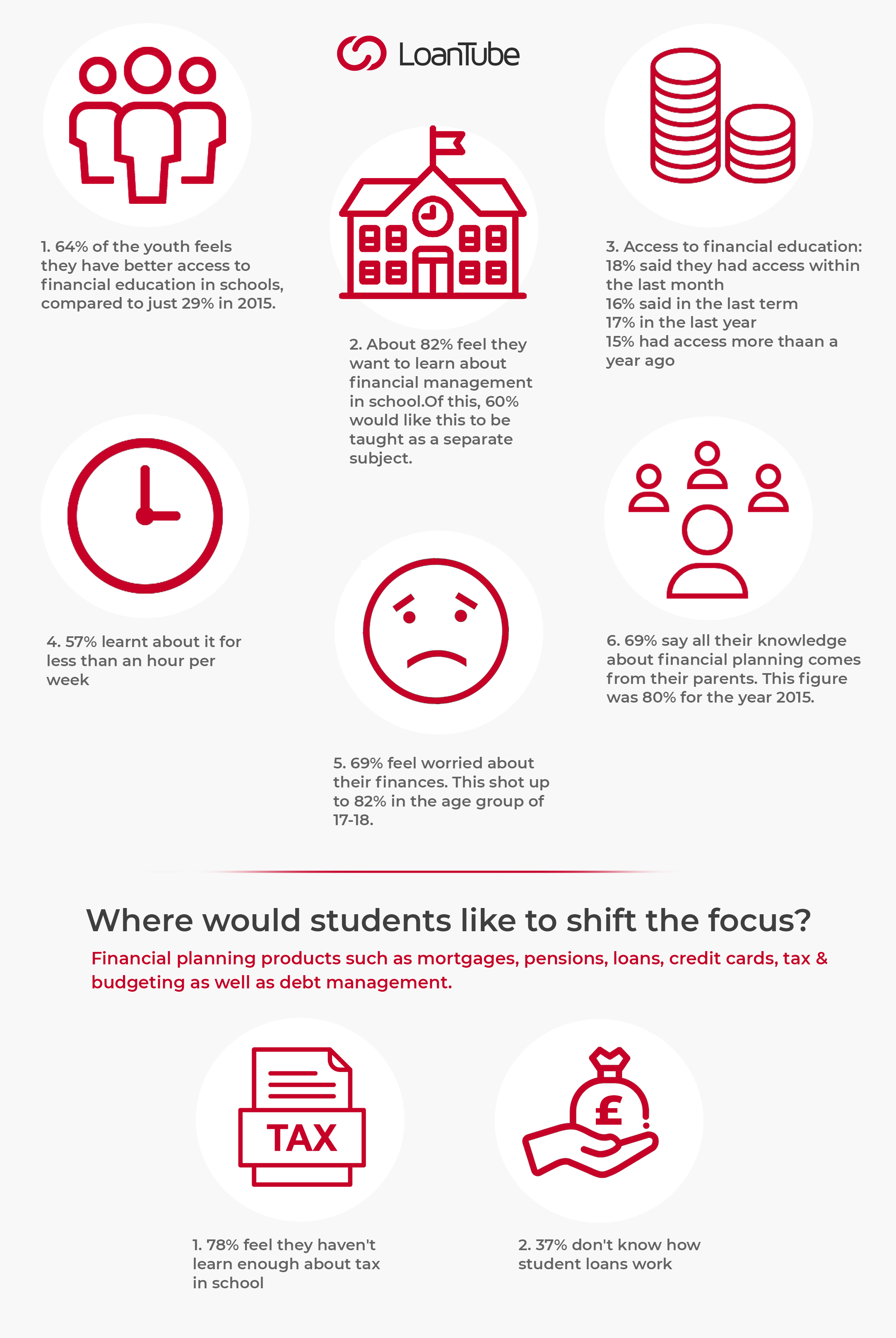

- Financial education access increased from 29% in 2015 to 64% in 2019. However, 86% of students stated that they learned financial skills from their parents or online rather than in school.

- While 42% of students want their parents to discuss money management, 82% prefer learning about it in school.

Financial Education in Schools: What’s Being Taught?

The UK introduced financial education into the national curriculum in 2014. According to the All-Party Parliamentary Group on Financial Education, the school syllabus covers the following topics:

Key Stage 1

- Identifying and understanding different coins and banknotes.

- Finding different combinations of coins to make equivalent values.

- Solving basic money-related addition and subtraction problems.

Key Stage 2

- Adding and subtracting money, including calculating change.

- Solving financial problems involving fractions and decimals.

- Estimating, comparing, and calculating different financial values.

Key Stage 3

- Understanding standard financial units such as income, expenses, and savings.

- Solving problems related to percentage changes in finances.

- Using concepts like unit pricing, compound interest, and debt repayment strategies.

Key Stage 4

- Calculating VAT and understanding tax obligations.

- Comparing different loan and savings options.

- Planning and managing personal finances effectively.

- Evaluating changes in income due to tax deductions and National Insurance contributions.

Improving Financial Education: What Needs to Change?

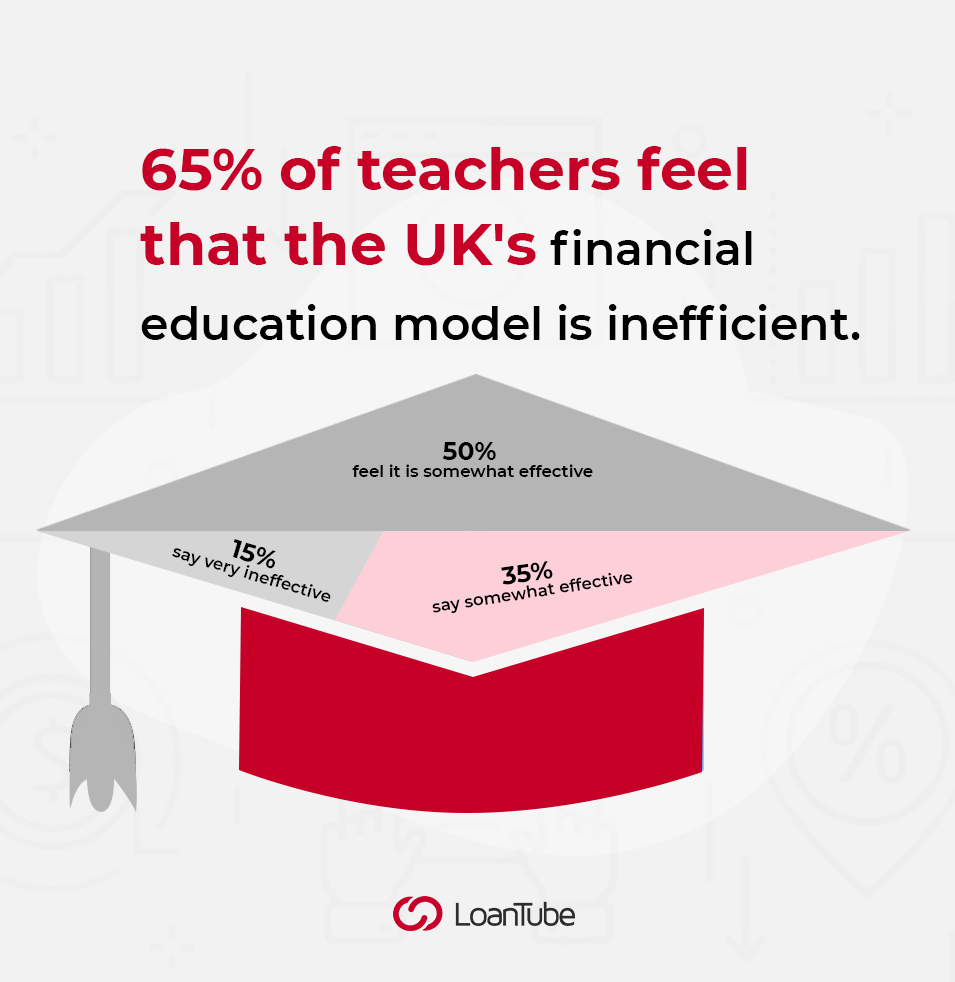

Many teachers feel that the current curriculum does not fully prepare students for real-world financial challenges. Given the rise in personal debt across the UK, enhancing financial education is crucial to preventing future financial hardships.

Strategies for Better Financial Education

- Encouraging Interactive Learning: Unlike traditional subjects, financial management requires hands-on experience. Schools can introduce real-life scenarios, interactive budgeting exercises, and engaging financial literacy games.

- Utilizing Free Learning Resources: High-quality, certified financial education materials can make lessons more effective and engaging.

- Hosting Guest Seminars: Schools should invite financial professionals to share their expertise and provide practical financial guidance.

- Focusing on Real-World Applications: Students need to learn about everyday financial topics, such as student loans, car financing, insurance, rent, and utilities.

Conclusion

A strong financial education system fosters responsible spending and long-term economic growth. The UK’s future depends on financially informed individuals who can make sound financial decisions. Schools must reinforce the importance of financial planning and money management.

Tackling financial illiteracy at an early age can help reduce long-term financial struggles. Teaching students how to balance spending and saving will enable them to lead more financially stable lives. If financial education is improved, future generations will have the tools needed to make informed decisions and avoid unnecessary debt.