We all love a Saturday night party with our friends. Getting sloshed is fun, and so are the hazy memories from an amazing night. But what happens when this habit starts affecting your financial life? Ever wondered how much you could save a year just by avoiding alcohol? Get a reality check through this article and learn more about the benefits of avoiding alcohol.

Britons are known to be YOLO spendthrifts. There’s one other thing that we’re famous for, and that’s our wholehearted love for alcohol. Britons spend a whopping £21.6 Bn on alcohol in the year 2019. Did you know that you potentially spend over £1000 on alcohol in a year?

We crunched some numbers and figured that if you were to start drinking from the age of 18 until you’re 80, it could cost you around £62000! This did not surprise us, because 64% of people admitted to borrowing money just to drink alcohol. Now for all we know, this could be a credit card debt or an overdraft. Regardless, the numbers are startling.

If you’re trying to quit drinking or motivating someone to limit their consumption, your instinct would be to list out the health benefits of quitting. Surprisingly, cutting down on alcohol won’t just make your healthier, but also yield you some savings!

To understand how avoiding alcohol can save you £1000s, you must learn how much you’re really spending on it.

How much does alcohol cost you per year?

Pubs are fancy, fancy places are pricey. The cost of a pint even at a basic London pub is expensive since there are taxes involved. An ONS statistic from 2019 indicates that an average Briton spends around £868 annually only on alcohol.

The report suggests a change in the trend of alcohol consumption concerning people’s income levels. People falling in the lower income bracket (less than £10000 in disposable income/year) spend around £6 a week on alcohol. On the contrary, the financially sustained spend around £35 a week. So, if you’re earning well, you are likely to spend 6.5 times as much on alcohol as someone with a low income.

No matter how well or little you earn, limiting your intake will financially benefit you in the longer run. Let’s take a look at the broader picture and examine how the impact of alcohol consumption on your life as well as the economy.

What does it cost the economy: The thought that those 5 pegs of whiskey that you consumed last week can have such an impact can be perplexing. The stats below will give you a reality check:

- Over 16 Million productive working days succumb to your hangover. This could cost your employer roughly £6.4 Bn a year.

- Students spend over £200 in pubs and clubs in the fresher’s week, during orientation. It’s thrilling at that moment but not when you’ve to pay the student loan back.

- Over the last few years, household spending on alcohol has drastically spiked. It’s grown from £18.2 Bn in 2015 to £21.6 in 2019.

What does it cost the consumer: The harrowing hangover that you experience the night after your boozy affair at the pub comes at a great cost. Take a look at the numbers below:

- 14% of women and 28% of men consume alcohol over the prescribed weekly drinking limit.

- In the year 2017, around 5,843 people lost their lives to alcohol. This is a 16% hike from the figure recorded in 2007.

- 54% of Britons spend over £60 a month just on alcohol.

- 64% of Britons admitted to using credit cards and bank overdrafts to buy alcohol.

- Three-quarters of Britons have, at some point, borrowed money from a friend or family member to buy alcohol.

Now we all know that on a night out with your brigade, alcohol is just one of the many things you spend on. But it is, however, the primary reason for you to go out.

The real cost of a night out

You may be under the impression that a night out is all about the money you spend on drinks. Sadly, that’s not the case. The hidden costs associated with a night out pile on quicker than you could fathom. Here’s how:

- Getting ready for the night out: Let’s admit it, we all want to look good when we’re drunk. We spend hours looking for the perfect Saturday night outfit and spend on dresses that burn a hole in our pocket. A lot of us aren’t keen on repeating our glamorous outfits. So we end up spending on a new dress every weekend, because why not? This spending pattern might prove detrimental to your finances as you may develop the habit of surviving payday to payday.

- Cost of commuting: When on a night out, you know you’re going to get sloshed. Most people don’t prefer to use their own vehicles on a night out. This could cost you anywhere between £60 and £80 for a round trip, depending on the distance. There’s a night charge on cabs post 9 pm. This is another cost that adds up to your alcohol expense pile.

- The hung-over mornings: Even those hung-over mornings cost you money. You won’t have the strength to cook or clean, so you’re probably going to spend more on a hefty brunch. Even a decent English breakfast at the café next door could cost around £15. Additionally, your supermarket purchases – an energy drink, Vitamin pills, and aspirin could hand you a £10 Tesco bill.

Sure it’s only £60 in the cab and £15 for the breakfast and £10 at Tesco. But this £85 is what you spend on this activity every week! Imagine if you would have added this money to a savings pot. You could’ve traded your old bed for a new, better one. After all, a penny saved is a penny earned.

How can limiting your alcohol intake save you money?

There are as many monetary benefits of avoiding alcohol as there are health benefits. We’ve listed a few of those to motivate you to see the bigger picture:

Monetary benefit

- Limiting your alcohol intake will reduce how much you spend on it.

- You can reduce major outlying costs – cab fare, take-away food, buying other people drinks.

- You won’t have to buy a Saturday Night outfit every week.

- The expense of hangover cures – food, medicine, and energy drinks will reduce drastically.

Health benefit

- High productivity and increase energy levels.

- Focus and clarity in your work environment.

- Better sleeping patterns.

- Weight loss.

- Better and healthier-looking skin.

- A new perspective on alcohol consumption.

- A sense of achievement and triumph for winning over an unhealthy habit.

Drink less, save more: Here’s how you do it

Finding motivation becomes easier when you accept a situation and are willing to work towards change. Here are a few tips from us to help you stay driven towards this goal:

- Take some dry days in your week, where you prohibit yourself from consuming any form of alcohol. Try a ‘two drinks per week’ policy.

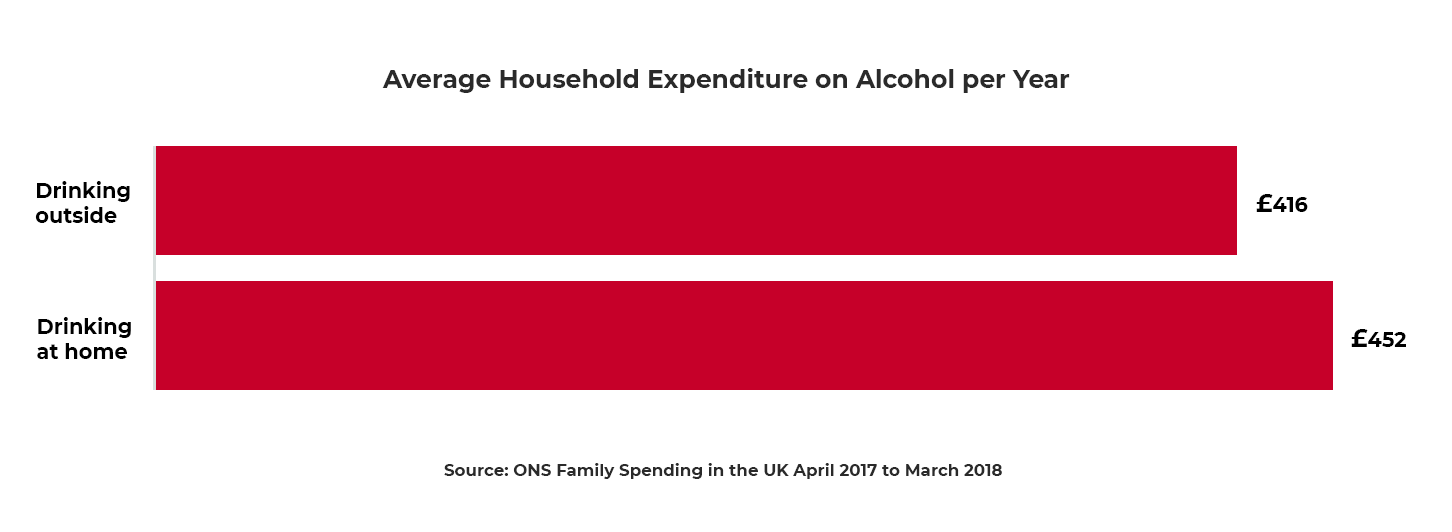

- Try to avoid drinking at home. If you can, stop drinking at home altogether. Reward yourself with alcohol only on the weekends.

- Try activities like Sober October and see how long you can last.

- If you feel that you need professional help, visit the NHS website, and find yourself some useful links and good advice.

A change in your habit can bring joy to those close to you. This could help you evolve into a better and more financially responsible individual.