Public finances have changed dramatically in the first quarter of 2020. As the pandemic continues to impact lives and finances, we are waiting for a fundamental shift. Is it the worst economic downturn?

The Coronavirus pandemic has put the global economy into great peril. But what’s more threatening is the fact that there is no certainty over the resolution of this health crisis. Despite all the support and funding initiated by the UK Government, people are being swallowed into the whirlpool of this financial crisis. Forecasters have predicted that a deep recession is underway. However, with ambiguity around the course of this pandemic, it’s tough to establish any facts. Therefore, we did a fact check in order to help you understand the intricacies of the current dynamic economy.

The Great Recession of 2008: Was that just a dry run?

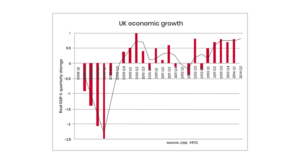

The Great Recession of 2008 marked the beginning of a 5 year-long period of a deep recession. This economic plunge commenced after a global credit crunch in 2007-2008, followed by a period of minimal or negative growth and higher rates of unemployment, across the UK.

The UK economy took a hit for 5 quarters in a row, after thriving with a whopping 63 quarter. It took five years for the economy to jump back to the size it was before the recession hit home. Between Q1-2008 and Q2-2009, the UK economy plummeted by more than 6%. During this recession, the unemployment rate rose to 8.4%, with close to 2.7 Mn people seeking work. However, even people earning a steady salary were struggling with making ends meet. Their income wasn’t enough to keep up with the increasing prices of goods and services.

The recession of 2008 in the UK, can be attributed to:

- Shortage of cash in banks, that led to a downturn in lending

- Low confidence of consumers and businesses, owing to the financial instability

- Fall in IMPEX, thanks to the vicious cycle of the global recession

- Housing Boom and Bad Credit

The housing boom was a period in which house prices grew rapidly, consequently leading to a growth in bank lending. Now with the increasing competition, banks were more than willing to take risks in lending. Owing to this, they relaxed their lending criteria and limited the checks on a borrower’s repayment ability. As a result of this, borrowers were left with a large repayment amount and inadequate resources to repay. This led to the loss of liquid assets for banks, who have now stuck neck-deep in this recession.

The Great Lockdown 2020: Drawing a comparison

The credit crash and recession of 2008 affected in the UK in ways that are yet to be fully discovered. Just as we started to recover from the previous crisis, this new wave of financial catastrophe jolted us. The Coronavirus pandemic is giving the great recession a run for its money. Back in the days, the government pressed all buttons to avert a deeper dive into recession, including Zero Interest Rates (ZIPR) and Quantitative Easing (QE). However, with the Covid-19 outbreak, there’s only so much they can do, given the vagueness and ambiguity around it.

Economies are drowning into this quicksand that Coronavirus is turning into. As a result, investors fear a decline that the government will not be able to avert. In response to this, Central Banks in the UK have slashed their interest rates to encourage borrowing and spending.

As the UK was forced to set a nationwide lockdown due to the pandemic, the economy shrank by 2% by March 2020. This means the virus had such severe implications, just within 3 months of exposure to it. While the analysts actually expected a decline by 2.6% in Q1-2020, this still remains the greatest contraction since 2008.

Some more facts about the Covid-19 economic fall:

- The Service Output, which comprises of retail, hospitality and travel, decremented by 1.9%.

- Household spending actually dropped by 40% in the month of April, as opposed to 30% suggested by the Bank of England.

- Approximately 15% of the people have witnessed a drop of over 50% in their income. People with lower incomes had to resort to borrowing after their savings were exhausted. This has led to an increased disparity between consumption and income.

- Over half-a-million people in the UK, applied for Universal Credit, within two weeks in March.

The pandemic has impacted multiple facades of our routine life. As we lose count of the things that will be adversely affected by this virus, we can’t help but wonder if the 2008 recession was merely a run-through for this outbreak.

What does the future hold?

With a number of businesses incurring great losses due to the Pandemic, jobs have drastically reduced in the UK job market. A huge section of people has lost their jobs to Coronavirus, while others are witnessing pay cuts due to decreased working hours. This decrease in income will have a significant impact on consumption, thereby leading to a sharp fall.

As this chain reaction continues, the Bank of England has predicted a contraction by 30% overall, in the first half of 2020. We have outlined some forecasts for the financial crisis of 2020:

- The inflation has been predicted to dip 0.5% in FY 2021, before bouncing back to the 2% target in 2022.

- UK companies that previously functioned with a cash flow deficit of £80bn, will now see a deficit of £190bn

- For this gap, the government would cover a major chunk. But banks will need to extend their support for the remaining 60bn.

- The Central Bank may provide more QE by August

- If high-street lenders fail to lend to their business customers, companies may collapse, leading to an increase of 2% in the shortage of job opportunities

- As a result, the GDP may drop by 13% as a whole for FY 2020

- The rate of unemployment could hit 10% by the month of June

After consistently working towards increasing employment, the UK government might see worse levels of unemployment compared to the levels during the 1990’s recession.

The government has set various measures in place to help businesses and employees sustain this situation. However, it goes without saying that 2021 will be a more cautious and risk-averting year, implying slower growth and lower inflation.

On the brighter side

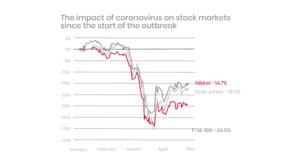

Amidst the strict lockdown measures, companies resorted to a ‘Work from Home’ environment for the smooth functioning of their business. Due to this, companies like Zoom, Amazon and Netflix hit a new high in the share market. Below is a summary of their growth so far:

- As a result of the increasing shift towards video conferencing, Zoom saw a growth of 131.1% in their share price.

- With the lockdown preventing people from stepping out, people are resorting to online shopping. The e-commerce giant Amazon witnessed an increase of 26.9% in their share price.

- When people are stuck at home, the demand for in house entertainment is bound to increase. Netflix takes the center stage with an increment of 28.9% in its share price.

As we find ways to keep ourselves occupied to get through this severe crisis, we urge you to be more open about your financial needs. Your financial instability can take a toll on your mental health. Therefore, it is important to take a reality check about your finances and address any issues. With a little help from LoanTube, you can fill those gaps and steal some peace from life, during these trying times. The recession that this crisis will bring is inevitable, but so is the growth in the economy once it passes. We cannot avert what’s ahead of us, but we can walk through it together.