Household debts are rising in UK. Read this article to know how secured debt and unsecured debt are connected to that.

[vc_row][vc_column][vc_column_text]

Money is something us Brits don’t like talking about. From our salaries to how much we paid for our new car, we tend to clam up when it comes to our finances. A recent report carried out by the National Audit Office has shed some light on this topic and uncovered some slightly worrying statistics when it comes to the state of the nation’s personal finances.

According to the findings, the average amount of household debt for 2018 currently stands at £58,540 and is made up of a combination of secured and unsecured debt.

Maximise your options: Compare and apply for loans below with LoanTube

Apply Filters

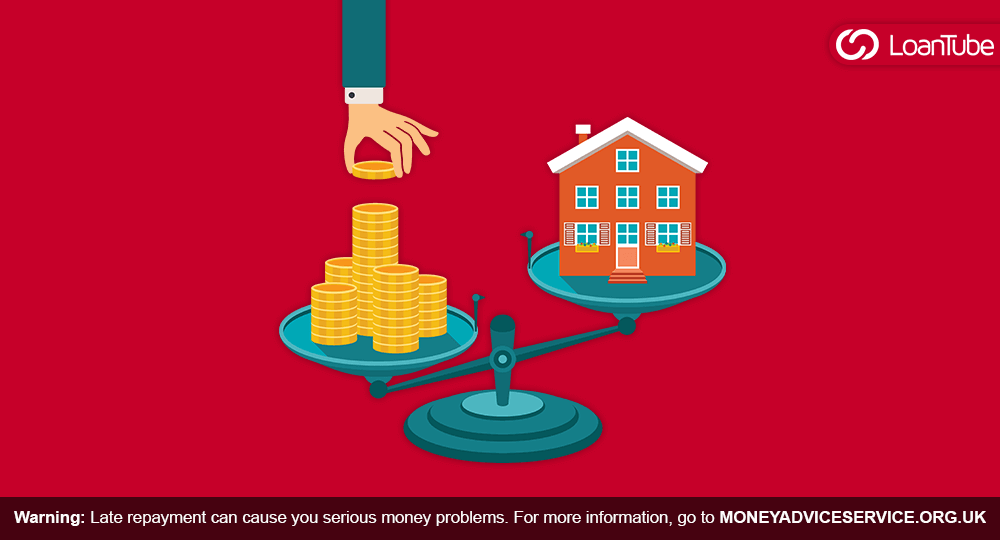

What’s the difference between secured and unsecured debt?

Secured debt is usually connected to an asset, such as a car or house, so think along the lines of car finance or mortgages. Unsecured debt, on the other hand, takes into account credit cards and personal loans not tied to an asset and usually come with higher interest rates. It’s not uncommon for many households to have borrowing across both types.

The amount of mortgage lending has dramatically increased by 7.6% over the last 12 months, and the value of spending on cards from high street banks also increased by a whopping 8.1% – this has been blamed on the warm summer and the World Cup of all things.

Shockingly, more than 8 million households are struggling to pay off household debt and bills and find themselves in a financial situation that can be challenging. Financial advice charities are calling for the Treasury to do more to help households better manage their finances and start to free themselves from the shackles of debt.

More going out than coming in

One concerning figure from the report highlighted that back in 2017; the annual outgoings of many people surpassed their earnings for the first time in 3 decades, with 619,000 contacting debt advice charity, StepChange.

Many of those seeking advice were under 40, showing that the younger generations were having the toughest time overcoming debt.

Interest rate concerns

With the Bank of England increasing their interest rates from 0.5% to 0.75% recently, this is a source of anxiety for individuals who are struggling to free themselves from difficult periods of indebtedness.

With Brexit on the horizon, a period of great uncertainty looms for the UK economy and financial markets, so less is most definitely more when it comes to household borrowing.

[/vc_column_text][vc_column_text]Source: Stepchange.org[/vc_column_text][/vc_column][/vc_row]